Following on from the previous post 6 Ways CBDCs could affect real estate investing forever, this week we will look at how you start protecting your wealth in the age of CBDCs.

Now, I don’t know about you, but my money is my money to do with how I wish. If I want to blow it all on a Pokémon collection, I will. (I wouldn’t actually). If I want to invest in real estate, equity index trackers or gold, I will. (I will actually).

What I resent is any government believing that they are entitled to take my wealth off me, either now or when I shuffle off instead of passing it on to my children. I believe CBDCs should be resisted for as long as possible and you should prepare for them now. This is how I believe CBDCs will affect how you will store your wealth in future.

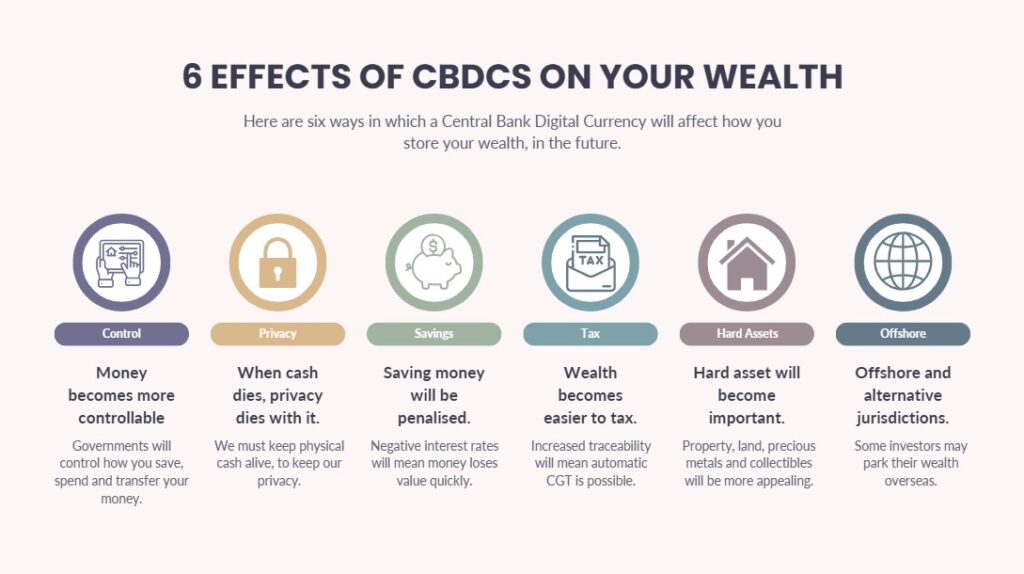

1. Money Becomes More Controllable

As we have seen in the post What is a CBDC and why it matters to everyday investors, they are programmable, traceable and will be issued by a central bank such as The Bank of England or the Federal Reserve. That will give governments more control over how money is:

- Saved

- Spent

- Transferred

They could, in theory:

Freeze accounts instantly

A government may freeze criminals’ bank accounts immediately. We know they do this with criminals’ assets now. What is to stop them from doing this to people who are just a political opponent?

Set expiry dates

Programmable money could have a set expiry date. Why would a government want to do that? Well, they may want to stimulate spending and drive up the economy, artificially, by forcing people to spend their money or lose it. This would discourage savings and make people more reliant on the state, which is their overall aim.

Restrict spending types

Programmable currency may also prevent someone making certain purchases. For instance, if a government wants to limit so-called vice spending, they might restrict or prevent spending on alcohol or gambling.

Apply negative interest rates

Another way of stimulating growth, by encouraging spending, could be to apply a negative interest rate. Therefore, the money in your digital wallet would reduce in real terms. This again would penalise high savings.

Implication

The implications of all this is that holding large sums in CBDC form may not be ideal for long-term wealth storage. The only use of CBDCs would be for, is for transactions. From this moment on if you don’t already, diversify your wealth storage into hard assets and alternative vehicles, such as property, commodities, businesses etc.

Disclaimer:

Just because I’m financially independent doesn’t mean you can sue me if you blow your savings on crypto llamas. This blog is for education and entertainment—not financial advice. Before making any money moves, speak to a qualified (and hopefully not-broke) Independent Financial Advisor. You know, the kind with certificates and a filing cabinet.

2. Cash Dies, Privacy Dies with It

We must keep physical cash alive. I cannot stress this enough. If as many people use cash now, we will incentivise businesses to continue taking it. We can punish businesses who don’t take cash.

The reason for this is that if physical cash disappears, then so does our ability to:

- Store wealth anonymously

- Make private transfers

- Hold value outside the system

My business is my business.

The effect of the death of cash will be to push high-net-worth individuals and freedom-minded investors to:

- Buy tangible assets (property, land, gold, collectibles)

- Explore digital assets (Bitcoin, Monero, privacy coins). These are decentralised.

- Seek decentralised finance (DeFi) options not tied to CBDCs

- Look into index funds and strong foreign currencies, which will provide stability.

This should therefore be the strategy, now, for freedom-minded individuals; start to invest in non CBDC stores of value.

3. Savings Will Likely Be Penalised or Disincentivised

As we saw before, with CBDCs, governments will have the ability to set negative interest rates. This means that money will lose value if it is left idle. Programmable rules could be used to discourage hoarding and therefore drive consumer spending.

This could mean that saved money in CBDC form will lose value over time.

“Money velocity” or how quickly money flows through the system will be enforced through policy, not just psychology.

What can you do about this now?

Your strategy should be to convert earned income into appreciating or income-generating assets as soon as possible. These assets would include real estate, dividend stocks, business equity. This is a common wealth accumulation strategy, anyway, but it will become more important once your country adopts a CBDC.

4. Wealth Becomes Easier to Track & Tax

If every CBDC transaction is recorded, then you can expect that the government will use the information to maximise tax revenues.

Automatic capital gains tracking will be possible and there will be full visibility of asset transfers.

There will be cross-referenced ownership registries, for example with property titles and digital ID.

You should therefore ensure you are compliant, now. Be vigilant about this as ignorance is no defence.

You can be proactive about this, by legally and transparently using trusts, corporations or investment vehicles, to minimise your tax burden. You’ve probably heard the saying from Claus Schwab “You will own nothing and be happy.” Well, I prefer building a tax strategy based on “owning nothing and controlling everything.”

5. Hard Assets Will Regain Importance

When digital money becomes easy to freeze, expire or be snooped on, then hard assets will become even more appealing. Some examples of hard assets are:

Property: This has a longstanding store of value and is also income-producing.

Land: Land, especially rural, agricultural or development land, will become increasingly valuable as a store of wealth. See my post The Future of Wealth where I discuss how natural resources are becoming scarce and will be monetised.

Precious metals: From time immemorial, precious metals have been a store of wealth. Gold and silver can also be held either physically or tokenised.

Collectibles: If you have an interest or passion, then collectibles will increasingly be a safe store of wealth. Examples are art, whisky, watches, etc.

See my post on portable property where I discuss what assets you could invest in for small sums now.

Strategy

Your strategy for using hard assets as a wealth store should be to balance liquidity and tangibility. This means you should only keep just enough CBDC for transactions. Any surplus wealth, you should store in durable, appreciating assets.

6. Offshore & Alternative Jurisdictions

As control increases domestically, some investors may seek to park their wealth in offshore or alternative jurisdictions.

There may be other overseas jurisdictions with more privacy or asset protection, than what your home country has.

Some investors may also store their wealth in foreign property investments. This would likely be in countries with low debt and sound currencies. This might be a wise choice if we see storms brewing at home.

Educate yourself on cross-border options, for real estate, banks and wallets; Make sure you have a Plan B wealth strategy.

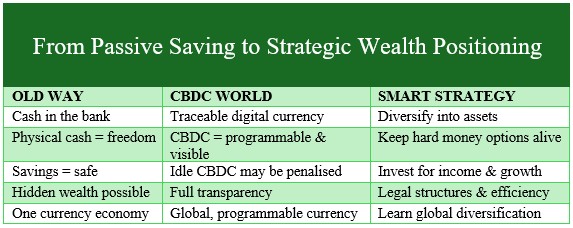

Summary: From Passive Saving to Strategic Wealth Positioning

If you think about it, CBDCs are not just a change in money, they are a change in power. The winners will be:

- Those who adapt to them early

- The people who understand the shift from saving to positioning

- Those who stay calm, strategic and focused on value, not currency

We have three choices, about how we move forward in this new unchartered territory. The first way is to bury our heads in the sand and hope it doesn’t happen. Next, we could try to fight the system. To me that would be energy sapping. Yes, we should vote against it, but the best option is to plan for a world, in which we have the power.

Stay on the look out for future posts in this series as I will talk more about where you can place your wealth and to keep yourself safe, in control and to maintain your anonymity. Sign up for the newsletter to make sure you don’t miss out.