I can’t remember the very first time I spent some cash. It was the early 1970s, though, as I was probably very young. It must have been a profound experience and although it hasn’t survived my conscious memory it most certainly is engrained in my subconscious. I must have realised that if you give the man in the sweet shop some small round metal discs, you were allowed to take the penny chews and gob stoppers away, with out him shouting at you.

Those round metals discs represent a medium of exchange that has evolved through 1,000s of years from barter, salt (that’s where we get salary from), through to these precious metals to promissory notes. Money continues to evolve, the move to a cashless society has accelerated since the lockdowns.

Digital transactions are convenient and easy. Money just like water (current/currencies/liquidity) likes the path of least resistance. So, we hurtle towards a time where those bits of metal and paper become antiques to be collected but not used.

While a completely cashless society is not an immediate certainty, the move towards digital payments is accelerating. Are there any benefits to it? As a Gen Xer myself my life straddles two eras – pre and post digital. I’ve embraced modernity (most of it) and I do see the benefits of digital money:

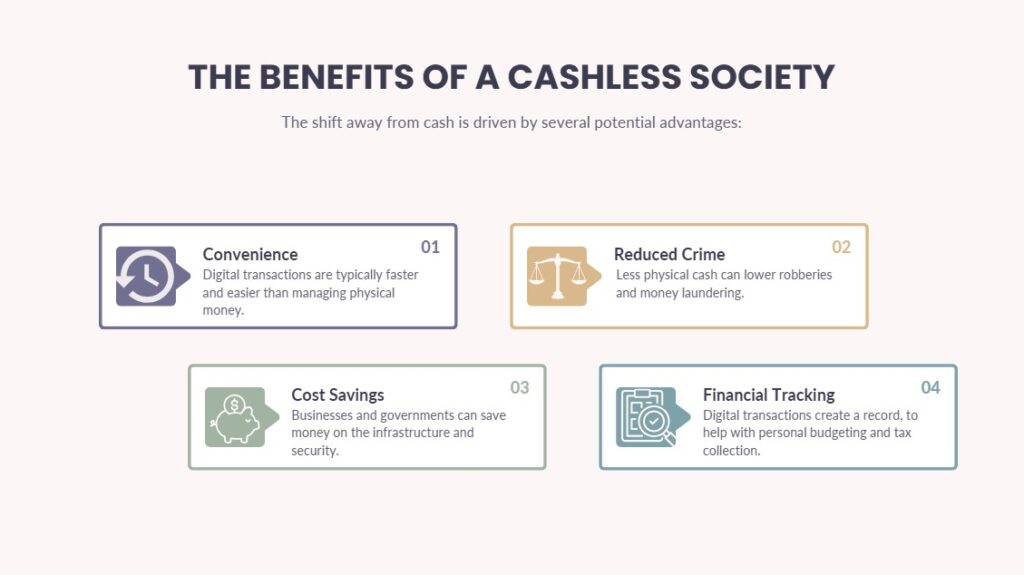

Benefits of a cashless society

The shift away from cash is driven by several potential advantages:

Convenience

As I said before money follows the path of least resistance and digital transactions are typically faster and easier than managing physical money.

Reduced crime

Less physical cash in circulation can lower the risk of robberies and make large-scale criminal activities like money laundering more difficult to hide from authorities.

Cost savings

Businesses and governments can save money on the infrastructure and security associated with producing, transporting and managing physical currency.

Better financial tracking

Digital transactions create an automatic record, which can help with personal budgeting and tax collection.

Potential drawbacks and how to prepare

However, as with any upside there is always a downside. A transition to a cashless system also presents challenges that you can prepare for:

Financial exclusion

Individuals without bank accounts, reliable internet, or familiarity with digital technology (such as the elderly) could be left behind. To mitigate this, some financial products like prepaid cards can be used as an alternative to a traditional bank account.

Privacy concerns

Every digital transaction leaves a data trail that can be monitored by companies and governments, raising issues around personal privacy.

System failures

A digital-reliant system is vulnerable to power outages, cyberattacks, or network failures that could make transactions impossible. Having backup payment methods on different networks (e.g., Visa and Mastercard) can help.

Risk of overspending

Digital payments make spending effortless, potentially leading to a disconnect from the financial consequences and increasing the risk of debt. Budgeting apps can help you track spending in a digital environment.

How to prepare without panicking

Instead of fearing the future, you can take practical steps to secure your finances:

Disclaimer:

Just because I’m financially independent doesn’t mean you can sue me if you blow your savings on crypto llamas. This blog is for education and entertainment—not financial advice. Before making any money moves, speak to a qualified (and hopefully not-broke) Independent Financial Advisor. You know, the kind with certificates and a filing cabinet.

1. Build a robust emergency fund

Create a separate interest-bearing savings account with three to six months’ worth of living expenses. This provides a safety net for unexpected events without resorting to credit or high-interest loans.

2. Diversify payment options

Ensure you have access to multiple non-cash payment methods. Consider having cards from different payment networks (like Visa and Mastercard) in case one system fails. Explore digital wallets and peer-to-peer payment apps as alternatives. See my post Crypto for Beginners: How to Use Cryptocurrency for Wealth Protection, Not Speculation. In that post I walk you through how to get started with crypto.

3. Enhance your financial literacy

Learn about online banking, budgeting apps and managing debt and savings in a digital-first world. This knowledge helps you gain confidence and control over your finances.

4. Protect yourself from cybercrime

In a digital economy, you are more exposed to hacking and fraud. Use strong passwords, two-factor authentication and virtual cards to protect your financial data and accounts.

5. Keep physical records

While less crucial than in the past, keeping paper copies of important financial documents can provide a reassuring safety net in case of a technological error.

The Question Mark in the Title?

So, the title of this post is The End of Cash? , with a question mark. I personally think that cash will not disappear. There are enough people who will resist its removal. Yes, it will be used less but there will always be some companies who will still accept it. They will be rewarded with my cash.

As I said in a previous post What is a CBDC and Why It Matters to Everyday Investors, there will be four types of currency: Cash; Commercial Bank Digital (your bank account/ debit cards etc); Central Bank Digital Currency; Cryptocurrency. In that post I also explain why you should hold all four (when CBDCs do arrive) and, as entrepreneurs, be set up to receive them.

I’ve also not talked about the barter economy and fair exchange transactions. I will in future posts, though.

Summary

The shift toward a digital-first financial world doesn’t have to feel like the ground is moving beneath your feet. Cash may fade in day-to-day use, but it isn’t vanishing overnight. Those who stay adaptable, informed and diversified will navigate the transition with ease.

Think of this period as a crossover decade: analogue roots, digital acceleration, and new forms of money emerging side by side. By strengthening your financial toolkit now, from emergency buffers to cyber-smart habits and a mix of payment options, you put yourself in a position of control, not concern.

The future of money isn’t about panic; it’s about preparation. If you’re ready, in the next post I’m going to take a deeper look at programmable money and what it could mean for your freedom. Sign up so you don’t miss out.