It doesn’t matter who wins the election and in this post I explain why.

“The idea that you can vote yourself into prosperity is one of the of most ludicrous that was ever entertained.” Winston Churchill

Clear, practical steps to build wealth, protect it and get your freedom back sooner than you think.

It doesn’t matter who wins the election and in this post I explain why.

“The idea that you can vote yourself into prosperity is one of the of most ludicrous that was ever entertained.” Winston Churchill

My lead content type is writing. It is what is natural for me, I’ve always written and it was what I excelled at, at school. Repurposing content allows me to get me writing out to more platforms and drive traffic back to my blog.

Routine Machine by John Lamerton is chock full of ideas and tips to help you improve your habits in all facets of your life, especially business and health. Here are the 17 key takeaways I got from reading it.

Continue reading “Routine Machine by John Lamerton – my 13 Takeaways”

This post was going to be about the best books on Time Management and getting things done. As I was looking through my library and thinking about the books I’ve read, Getting Things Done by David Allen would be the top of the list. Then I realised that this is the only book on time management you need. If you’ve not yet read Getting Things Done, then read on and I explain why.

Continue reading “Getting Things Done by David Allen – Book Report”

Creating content, has many great benefits for business and for providing a creative outlet. To get the best benefit out of it, it should be done consistently. Daily if possible. When is the best time for creating content, then? I’ve experimented with various times and here is what I’ve found.

Continue reading “When is the best time for creating content?”

I practice the GTD system of Getting Things Done by David Allen. The beauty of it, is that you can tailor it to your own needs. One thing that I’ve played around with, is what to do with recurring tasks. Recurring tasks are those items that repeat every day, so how do you record this on a to do list. Here are some ways in which I’ve tried to record recurring tasks.

“The person with dreams is more powerful than the one with all the facts” – Albert Einstein.

I’m sure Einstein was talking about those dreams which are our hopes and aspirations, rather than what goes on when we are asleep. I would like to posit that those movies we play when we are unconscious are important. Therefore, you should record your dreams so that you may benefit from them.

The older I get the more I realise the importance of sleep. When you are younger you can afford to burn the candle at both ends, but eventually there comes a point where you must take sleep seriously.

As with all history, we are not just reading about dates and events, but we can also learn from the characters. We can take their virtues and avoid their vices. Here are some of the things I learned whilst reading Churchill’s books.

Continue reading “What I learned from reading Churchill’s Books”

If you are like me, you didn’t learn about personal finance at school. Your parents hopefully gave you a few nuggets of good advice around living below your means and saving for a rainy day. Everything else you may have learned about money you may have picked up from society and the media.

As you are reading this blog, you are obviously searching for answers to life’s questions as I was – and still am. Books remain, the best source of advice along with trusted mentors and coaches. Over the years I’ve read thousands of books on personal development, finance, sales and business. Out of all the books I’ve read on personal finance here the ten which I believe are the best to start you on your quest.

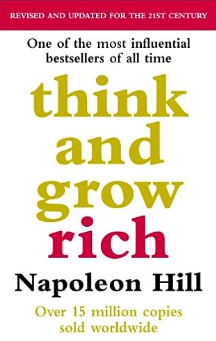

Hill wrote Think and Grow Rich in the early 20th century and it remains a classic guide to getting the right mindset around earning money by providing some kind of service.

The author was asked to draft the book by his mentor, the great industrialist Andrew Carnegie. Hill then spent the next 20 years studying the great wealth producers of the time. He then distilled all he learned into this book.

The introduction starts with the teaser, that the secret to riches is mentioned in every chapter. You are asked to read and reread the book, to let its messages sink in.

20 years after I first read this book, I still make sure I reread it every year.

Rich Dad, Poor Dad was the second book I read on money, shortly after reading Think and Grow Rich. The first reading of the book made me angry. Yes, I was furious. Not because of Kiyosaki’s style but because he made me realise that what society tells you about money is incorrect and in some cases very damaging.

The book is semi-autobiographical in that it shows how a young Robert first learns that his friend Mike’s dad is very wealthy and has a completely different philosophy around money compared to his real dad. Robert loved his real Dad but stated that he had followed the traditional route of Education – Job- Pension. When Real Dad realised his pension wasn’t going to support him, he belatedly looked at business as an option. Unfortunately, he was lacking in the skills after spending his career working for local government.

This book really changed my outlook on therefore my habits. From paying yourself first to producing your own monthly cashflow statements, these habits have helped me get to a point of financial independence.

My big takeaway from this is that you should take responsibility for your own financial education as early as possible. Get a job to gain knowledge and experience, so you can eventually start your own business.

The Cashflow Quadrant expands on the themes in Rich Dad Poor Dad and is a more practical ‘How to’ book. It introduces the four quadrants of financial outlook:

E – Employee. The place where most people start (and usually stay). You get a job, earn a wage and hopefully save enough for retirement, without getting downsized.

S – Self-employed. Here the technician goes it alone. They are master of their own destiny and have the benefit from a tax point of view. The downside is they are still tied to the business. I.e. if they don’t work, they don’t earn.

B-Business owner. People in the B quadrant have learned the art of leverage. They have set up systems and teams of employees who do the work. The measure of how successful the business owner is, is how long they can stay away from the business without it falling apart. They work On the business, not In the business.

I-Investor. A person in the I quadrant invests in other businesses. They may have been a successful Business owner who sold their holdings and now reinvests their profits for higher returns.

The premise of Your Money or Your Life is that every pound you have in your net worth represents an amount of time you don’t need to work. Using the rule of 4% Ie take 4% of your net worth and this is the amount you can live off per year which will ensure your nest egg doesn’t deplete and keeps pace with inflation. This is providing you invest it in the appropriate vehicles – the book describes what these are.

Conversely, every pound you do spend is a pound you don’t add to this savings pot and therefore is time you must keep working. For instance, say you spend £1,000 per year on your annual holiday. That would equate to £25,000 you need extra in your financial independence pot to be able to pay for this every year. (£1,000 is 4% of £25,000). Let’s say you earn £25 pounds per hour. That means you will have to work an additional 1,000 hours in your life to afford to take a £1,000 holiday per year. (More if you consider tax).

You should therefore question your spending and ask if each item or service you receive is worth the amount of extra time you would need to work. Let’s look at our holiday example again. For you, it might be non-negotiable that you want an annual holiday every year and so those extra hours work would be worth it.

If you go through this exercise with all your expenses, you will get a feel for what things in life, you buy, that give you true value.

As I approached Financial Independence and studied more on the subject, I came across the FIRE movement. FIRE or Financial Independence Retire Early, says that once you build up a net worth, of which a 4% withdrawal rate is enough to life on, you are free to retire (see no. 4) . The Early part of the equation states that you can cut your expenses to such a level that your net worth number doesn’t need to be as high as you think.

Jacob Lund Fisker’s book describes how you can take this to an extreme level. It goes beyond frugality and doing simple DIY tasks to cut costs. This is a way of life. For me it goes too far, but for many people it can be a way out of the rat race.

The Millionaire Next Door isn’t a practical book as such, but is the result of an exhaustive survey on several thousand millionaires in the US. It breaks down how real millionaires live their lives, such as what they spend their money on. Do they invest? And in what? It even looks at trends such as when they met their spouse, to even whether they repaired old shoes or bought new.

The premise really is that you wouldn’t be able to spot a millionaire in the street as they don’t look stereotypical. They wear ordinary clothes, usually unbranded and they drive sensible utilitarian cars. The lesson is that if you are an aspiring millionaire, do you do what real millionaires do? If so, you too can join them.

The Richest Man in Babylon is a short book of fables about some characters in ancient Babylon, who have the same worries and aspirations around money as we do today. For instance, why certain people get rich, whilst others struggle month to month. Is there such thing as luck or are lucky people doing certain things to get in the way of opportunity.

It describes how these characters learn, from a rich man, some simple rich habits, that we too can start today. These include paying yourself first – allocate 10% of your earnings before you spend on anything else and put this away to save. Once this savings nest egg reaches a certain level, you can then invest it for further growth. The book warns us though to take advice off trusted and experienced experts before investing.

The Millionaire Fastlane goes against the grain of most personal finance books. Demarco is quite disparaging of the get-rich-slow school of thought. He shows us how he himself escaped the rat race by creating a business, rather than saving and investing.

I thought the NECST model of business, that Demarco advises, is particularly useful to evaluate potential business ideas. The NECST model asks us to analyse our opportunity to see if:

N – there is a Need. Will people buy what you’re selling.

E- how easy is to Enter this business? Ie the easier it is, the more competition there will be.

C- how much Control do you have? E.g. Do you rely on one platform owned by another company? Think Amazon, Google etc.

S- can you Scale your business? The more you can scale the wealthier you will be. Think McDonalds vs a single restaurant.

T – can you take your Time out of the business. How reliant on you is the business? Can you take a month’s holiday and the business will still be running when you get back.

Failsafe investing introduced me to the Asset Allocation called the Permanent Portfolio. Here Browne advises splitting your assets into four classes of equal amounts – Gold, Cash, Bonds and Equities. At the end of the first year your whole portfolio should have grown, but each class will have grown at different rates, fallen or stayed static. You would then adjust your asset allocation so that all four are at parity again.

Then just repeat this process every year and you will, Browne assures us, match the markets.

In effect this model ensures that you sell assets high and buy low. As each type of asset class performs differently in different markets, your overall portfolio should grow regardless of whether we are in high/low inflation or bull/bear markets,

Becoming Rich takes a magical stance on money management. I particularly found useful the money buckets system, which I’ve seen elsewhere but this one resonated with me.

Every time you receive money, whether it’s a salary payment, windfall or sale of an item you split it into 5 buckets with a ratio of 10:10:10:10:60

The key to this system and why it is magic (psychological) is that you are earning money for others as well as yourself. This seems to take away some of the guilt some people can have around earning money. Often, we have negative baggage around money, from things we picked up in childhood. If we can eliminate these negative beliefs, we open ourselves up to receive more.

Becoming Rich advises us to remove 10% of the money you receive and put it into a separate account for gifting. We can then use this money to give to worthy causes that we believe in. It shouldn’t feel like an obligation but if we can find a cause or causes that we emotionally resonate with, then we will feel positive about gifting.

Tithing has been practiced ever since money has been around. People have noticed that as you gift money, you receive even more. I’m not sure how this works but try it out for yourself.

Guilt around money is not the only negative emotion around money. Worry must be the second emotion to eliminate. Often, we worry that we don’t have enough or that we may be met by some financial emergency in the future. Setting up a separate savings fund is really an entry-level personal finance habit, but in this method, you remove 10% of the money on the day you receive it. Then put this into the savings account. It should be automatic and we should never dip into it for treats etc.

Use this fund as a buffer against the worry of future mishaps.

Another negative trait that blocks our abundance is the fear of losing what we have. By having a fun fund, we can spend money on ourselves guilt free. Here you have a finite amount of money you can do anything with. It’s a specific amount you know you can blow. On the other side, though, it will force yourself to feel good about spending some money. After all what’s the point of earning money if you can’t enjoy it now.

The Other fund can be for things like a debt repayment plan, investment plan, saving for a specific big-ticket item or whatever. You are free to decide.

You’ve allocated 40% of you income into specific buckets so you will need to live off the rest. This may be a challenge at first, but you can start off with smaller than 10% buckets and work up to it. What is important are the habits this process creates.

So, there are my 10 favourite personal finance books. Have you read any of them? Do you agree? What books have made an impact on your finances?

If you are just starting on your personal finance journey, I would recommend starting with the three that have had the most impact on my life:

Think and Grow Rich

The Richest Man in Babylon

Rich Dad, Poor Dad.