Dave Ramsey is one of the most well know teachers in the space of personal finance. I particularly like his no-nonsense approach. His financial baby step system is easy-to-follow and will allow you to become wealthy in short time.

However, is he right about what he says about debt?

What does Dave Ramsey say about debt?

Dave Ramsey takes a biblical stance on debt. He says that all debt is bad and the ‘borrower is slave to the lender’. Baby step 2 in his 7 steps shows his pupils how to eliminate non-mortgage debt, using the snowball method.

I particularly like the snowball method, because you can get some quick psychological wins by attacking the smallest debt first. I’ve written about this elsewhere. There is also a debt avalanche method which is different in that you will attack the debt with the highest interest rate first. Both methods have their merits and the avalanche method may be quicker in the longer run.

However, I agree with Dave Ramsey here, in that some early quick wins, with the snowball method, will be an encouragement to those who maybe feeling under financial strain.

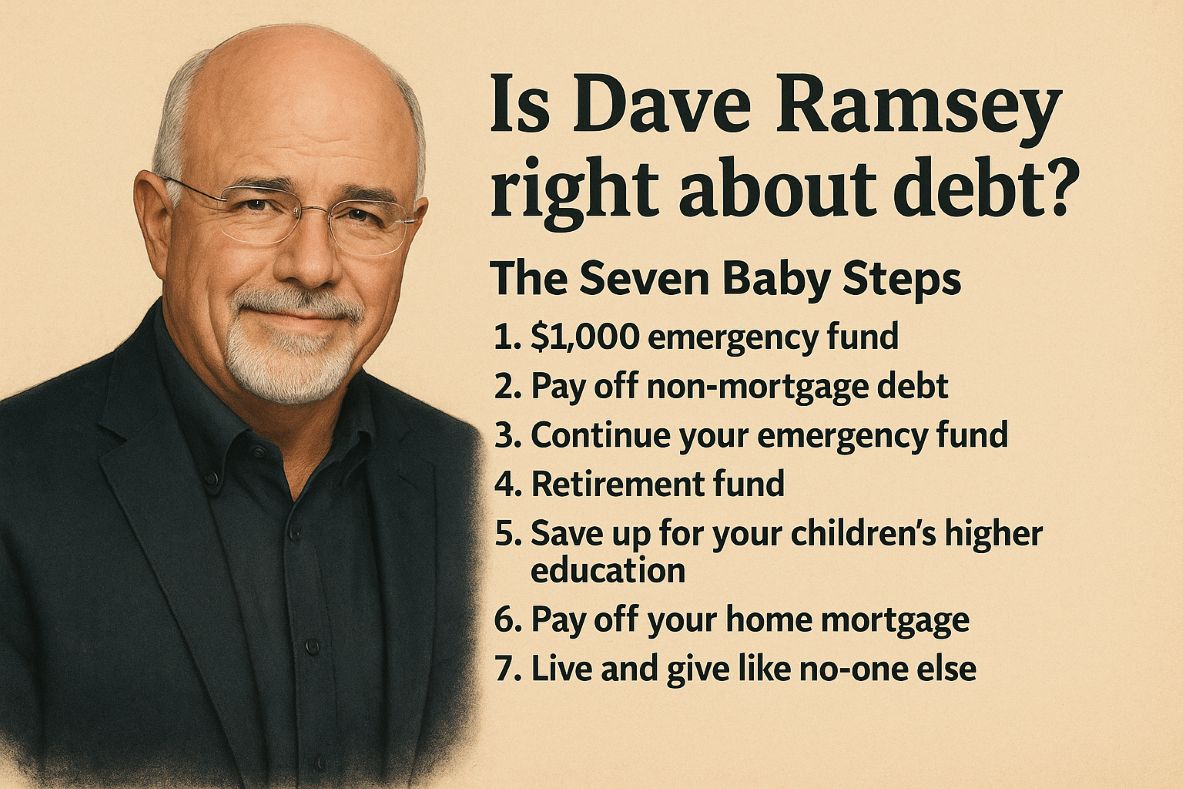

The Seven Baby Steps

As a reminder here are the 7 baby steps as taught by Ramsey. They are geared towards the US audiences but can easily be adapted to the UK reader. The important thing to remember is you must tackle each step, in order and not jump ahead. You can to tackle steps 4-6 at the same time though.

- $1,000 emergency fund. Save up $1,000 as an emergency fund. Often when people are in dire financial situation, they are hampered in their efforts to pay off debts and start long term savings plans. This is because some emergency will occur, which will eat up those funds. ‘Murphy will come round knocking’. This $1,000 fund, once saved, will act as your buffer against the winds of fate.

- Pay off non-mortgage debt. As I showed before, the next step is to eliminate all your non-mortgage debt using the snowball method. This will include loans. credit cards, store cards, overdrafts, car payments and student finance for the US. (Here I believe the UK student finance is a lot less onerous, so I wouldn’t include it in the baby steps).

- Continue your emergency fund. Once you remove all debt, use your increasing leftover income to continue saving for emergencies until you have 3-6 months of living expenses saved.

- Retirement fund. When you complete steps 1-3, direct at least 15% of your income into a retirement fund. Dave Ramsey talks about the US market here, but in the UK, this would be, for instance, a company pension scheme or personal pension. Make these payments automatic and continue for as long as you work.

- Save up for your children’s higher education. Alongside your 15% retirement fund, direct a percentage of your income into a separate investment account, which when mature, will be able to pay for you kids’ higher education. Quite rightly they will not have to get themselves into debt to study. Again, I’m not sure this is applicable in the UK. I would take advice on this.

- Pay off you home mortgage. Alongside steps 4 &5, start overpaying on your home mortgage, so that you can pay this off many years early.

- Live and give like no-one else. Now you have completed steps 1-6, now it’s time to enjoy your money. At this stage, you have cleared your debts, you have some set aside for emergencies, your retirement and child’s education. Now you can cruise to generational wealth.

When is he right?

I love this system, but I would say that there is maybe a step 0 missing in that the first step should be to get some income in the first place. But that aside, I agree.

Certainly that $1,000 emergency fund is a great way to stop living hand to mouth and if someone has never had this buffer before, it must be a god-send.

It goes without saying that I agree with saving for your retirement, future wealth and helping your offspring.

I also agree that you should remove all consumer debt, as quickly as possible. In fact, I’m in total agreement with Dave, not to have any consumer debt at all.

When is it not right?

Dave Ramsey states that all debt is bad, however he does acknowledge that you can use a mortgage to purchase a home, at around the time you are at step 4. My problem with the maxim that ‘all debt is bad’, is that it doesn’t differentiate between good debt and bad debt.

Bad debt is any debt that is used to purchase items that depreciate in value or consumer debt. Good debt therefore is debt that can be used to purchase items that appreciate in value and provide an income. Examples of good debt could be a mortgage to purchase a home, a mortgage to purchase a rental property or a business bank loan. The latter two forms of borrowing are called leverage and are legitimate forms of finance.

Conclusion

Where I think Dave Ramsey is coming from, by saying all debt is bad, is that his target audience are people who are in a financial mess. They might also be just starting out on their financial journey. I agree that all consumer debt is bad and you should avoid it like the plague.

Good debt in the hands of a novice, or someone who cannot manage their finances, could quickly turn into bad debt. Rather than make this differentiation, Ramsey safely errs on the side of caution.

I would say that for most people on the baby steps journey, they should avoid any further debt apart from the home mortgage. If they have safely navigated their way through the 7 steps, then they have demonstrated that they have learned the financial skills required. They could then take on good debt to accelerate their wealth. If they haven’t learned these skills then, yes, Dave Ramsey is right – all debt is bad.