In an earlier post in this series on the Future of Money – What is a CBDC and Why It Matters to Everyday Investors, I introduced the concept of programmable money. Programmable money is digital currency with built-in rules that can automate transactions based on predefined conditions.

This technology presents a significant duality, for personal freedom: It could enable new forms of economic autonomy and efficiency, however, it also poses a serious risk in terms of surveillance, control and reduced privacy. If not implemented with strong safeguards I believe it could be dystopian.

In this post I will go into more detail on what programmable money is and why we should be concerned but open to opportunities.

Potential Benefits of Programmable Money

1. Automated control

Programmable money could give users fine-grained control over their finances. For example, a parent could program pocket money so that their child can only spend it on school supplies and prevent other purchases.

2. Trust and efficiency

Smart contracts can reduce counterparty risk by automatically executing payments when agreed-upon conditions are met, such as confirming delivery of a product.

3. Financial inclusion

By reducing the cost of transactions and making financial services more accessible, programmable money could provide banking and investment opportunities to underserved populations.

Examples of programmable money

At its core, programmable money combines digital currency with logic. (If-This-Then-That). They will use smart contracts on blockchain technology. This embedded logic means that payments can be self-executing once specific conditions are met, eliminating the need for intermediaries.

Here are some of the other ways that organisations are exploring programmable money:

1. Business and corporate finance

Automated payroll

Companies can use smart contracts to pay salaries, automatically, on specific dates, which helps reduce delays and manual errors.

Treasury management

Programmable money allows for automated liquidity management, with funds being moved between accounts based on predefined thresholds and market conditions.

Business-to-business (B2B) payments

Conditional logic can automate B2B payments, with funds released only when conditions, such as delivery confirmation or invoice verification, are met.

Trade finance

The traditional process of managing payment instruments and trade documents can be streamlined, with payment and trade data integrated into a single programmable instrument. This can reduce discrepancies and speed up transactions.

Royalty payments

In the creator economy, royalties can be automatically distributed to rights holders as revenue comes in, ensuring fair and instant compensation for collaborators.

2. Supply chain and trade

Supply chain payments

Payments can be triggered automatically when goods are scanned at delivery points, confirming receipt and settling the transaction instantly.

Escrow services

Programmable money can function as a trust-less escrow, with a smart contract holding funds and releasing them automatically upon the fulfilment of predefined terms.

Trade finance and logistics

Payments can be automatically triggered only when goods arrive at the port or other delivery locations.

3. Government and public sector

Targeted aid

Governments can distribute financial aid or subsidies that are restricted to specific categories, such as groceries or education and released only when certain conditions are met.

Tax collection

Authorities could programme Central Bank Digital Currencies (CBDCs) to automatically deduct and pay taxes on certain transactions, improving compliance.

Emergency aid

Programmable CBDCs can enable the rapid and traceable disbursement of funds to affected regions during natural disasters.

Green stimulus

Governments could issue programmable money specifically earmarked for climate-friendly purchases, like electric vehicles or solar panels.

4. Consumer finance and other sectors

Conditional payments for online purchases

A buyer’s payment can be programmed to release to the seller only after the buyer confirms the goods have been received, helping to prevent fraud.

Insurance payouts

In parametric insurance, a claim can be automatically paid out by a smart contract when an external data source, or “oracle,” verifies the conditions have been met, such as a weather event triggering a crop insurance pay out.

Automated savings and investments

Funds can be automatically allocated from pay cheques to savings or investment accounts based on spending patterns or market changes.

Loyalty and rewards programs

Brands can issue loyalty tokens that are easy to track and manage, with programmable rules for expiration or evolution.

Fractional ownership

Real estate or other high-value assets can be tokenised into smaller, programmable units, making fractional ownership more accessible.

Implications for Personal Freedom

So, as we can see above there are a myriad of uses for programmable money and it is only limited by our imagination. But should we be concerned, after all, surely its progress?

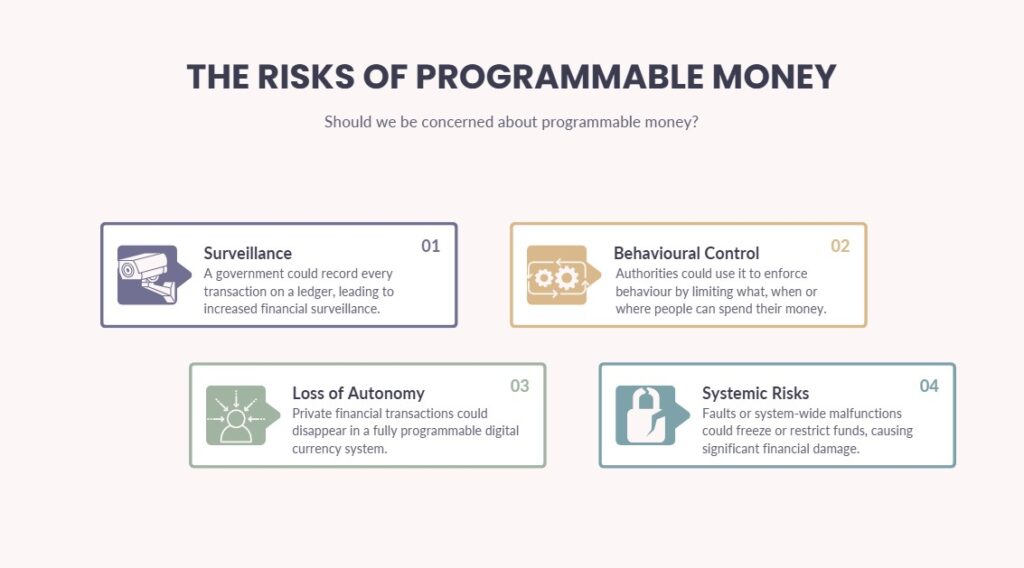

1. Surveillance

A government could record every transaction on an accessible ledger, potentially leading to unprecedented levels of financial surveillance. In the context of a Central Bank Digital Currency (CBDC), this raises concerns about privacy and how they monitor spending behaviour.

2. Behavioural control

Authorities could use programmable money to enforce behaviour by limiting what, when or where people can spend their money. Examples include implementing expiration dates on funds or restricting purchases to certain categories. This shifts money from a neutral instrument to a tool for behavioural governance.

3. Loss of autonomy

The ability to have private financial transactions, currently offered by physical cash, could disappear in a fully programmable digital currency system. This could create a two-tiered system where economic control is codified into everyday transactions.

4. Systemic risks

Faults in the code of smart contracts or system-wide malfunctions could freeze or restrict funds, causing significant financial damage. If not properly designed, programmable money could also interfere with payment autonomy.

The Ongoing Debate

The extent to which we realise these risks to our freedoms, depends heavily on how we govern the technology. For example, the European Central Bank has stated that a digital euro would aim to replicate the privacy of cash, not limit how individuals spend their money. Conversely, critics warn that without democratic oversight and strong privacy safeguards, programmable money could become a tool for excessive state control.

As central banks and fintech companies continue to explore this technology, transparency and public input will be crucial to establishing trust and setting clear limits on its use.

Programmable money is coming, whether we like it or not. Its potential to streamline life, widen access and cut out friction is real. However, so is its capacity to shrink personal freedom if left in the hands of unaccountable institutions.

The key here is to stay alert, informed and involved. We don’t need to fear this shift, but we do need to shape it. If we push for transparency, insist on proper safeguards and build our own parallel strategies for financial independence, programmable money can evolve into a tool that works for us, not one that quietly erodes the freedoms we rely on.

In the next post I will look at the sister to programmable money: Smart Contracts and how these will affect real estate entrepreneurs. Stay tuned.

In this next post in the blog series – The Future of Money, we open a new section which gives practical strategies for building wealth. The first raft of posts lay the groundwork of knowledge around how finances and the world of money will change, and is changing now. One pillar of wealth is the asset class property, so today, we will specifically look at how to build a CBDC resilient property portfolio.

My first fear when I heard about the onset of Central Bank Digital Currencies is they will be used by governments to snoop on us and try to nudge our behaviours around our spending habits. This is not to mention the potential for a government to try to punish certain spending and de-bank certain individuals. This happens, in places that already have a CBDC. So, in this next post in the series of the future of money I talk about how to stay free, flexible and financed in a CBDC world.

In the previous post in this series of the future of wealth I discussed ways in which you can protect your wealth in the coming Central Bank Digital Currency CBDC era. One of the ways we looked at was moving any surplus CBDC money as soon as possible into appreciating or income producing assets as soon as possible. Alternatively, you could convert this money into a form that at least holds its value relative to inflation over time. Therefore where should you store your wealth in the CBDC era?

In this latest post in the series The Future of Money, I look at how CBDCs could change real estate investing.

I, along with many people of my generation, am completely opposed to the introduction of a Central Bank Digital Currency, for reasons which I will lay out in a later post. However, we still need to educate ourselves about what they are, how they will affect us and how we can prepare for them if they do come.

So here I set out six ways in which they might specifically affect property and real estate investors.

In this latest post in the Future of Money series I look at how entrepreneurs can prepare for the CBDC era. In the last two posts I explained how and why the future of money is changing and what Central Bank Digital Currencies (CBDC) are.

In this second part of the series The Smart Start Guide to Wealth in a Digital Age, I will explore what a Central Bank Digital Currency or CBDC is and why it should matter to everyday investors.

Part One in the series: The Smart Start Guide to Wealth in a Digital Age

A few weeks ago, I was at the bar of a local pub. We’d just taken our dogs on a 10k walk in the heat, and everyone needed refreshments. My wife and the dogs were in the beer garden enjoying a well-earned rest, while I was ordering some refreshments.