There is one last job to do before you start searching for properties in your Goldmine Area. This is to choose your Mortgage Broker.

Choosing Your Mortgage Broker

Clear, practical steps to build wealth, protect it and get your freedom back sooner than you think.

There is one last job to do before you start searching for properties in your Goldmine Area. This is to choose your Mortgage Broker.

Are you ready to start building your property portfolio? The very first step is to work out where your goldmine area will be. In this post I go through a step by step process to help you find your goldmine area.

I’ve written several posts and even a book on how to retire early, or the Financial Independence Retire Early movement (FIRE). In July 2023 I finally reached the position whereby I didn’t need to work again. However, the feeling didn’t last, and I was back at work withing 3 months, although I was working for myself. You see, I decided that I won’t retire.

Reading You Will Own Nothing by Carol Roth, certainly is a journey. It is a scary journey, but one which could have a happy ending. You will decide how your ending turns out.

Continue reading “You Will Own Nothing by Carol Roth – my takeaways.”

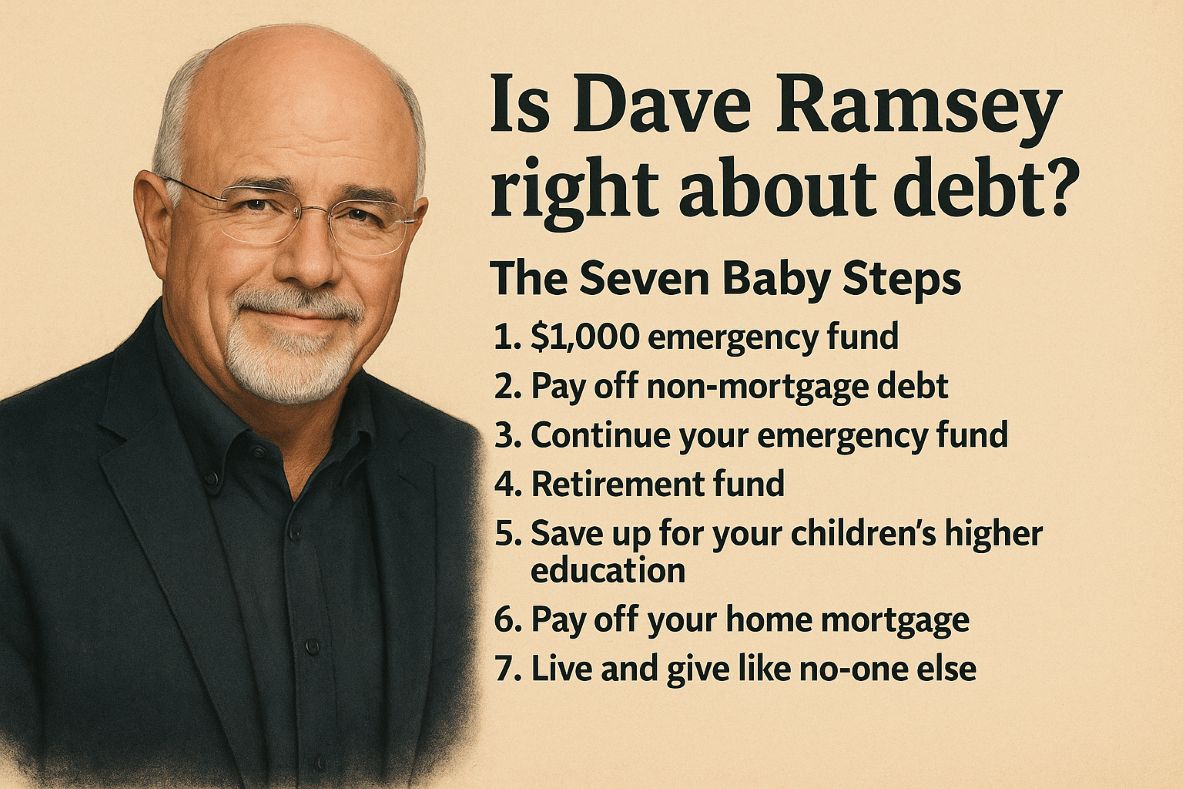

Dave Ramsey is one of the most well know teachers in the space of personal finance. I particularly like his no-nonsense approach. His financial baby step system is easy-to-follow and will allow you to become wealthy in short time.

However, is he right about what he says about debt?

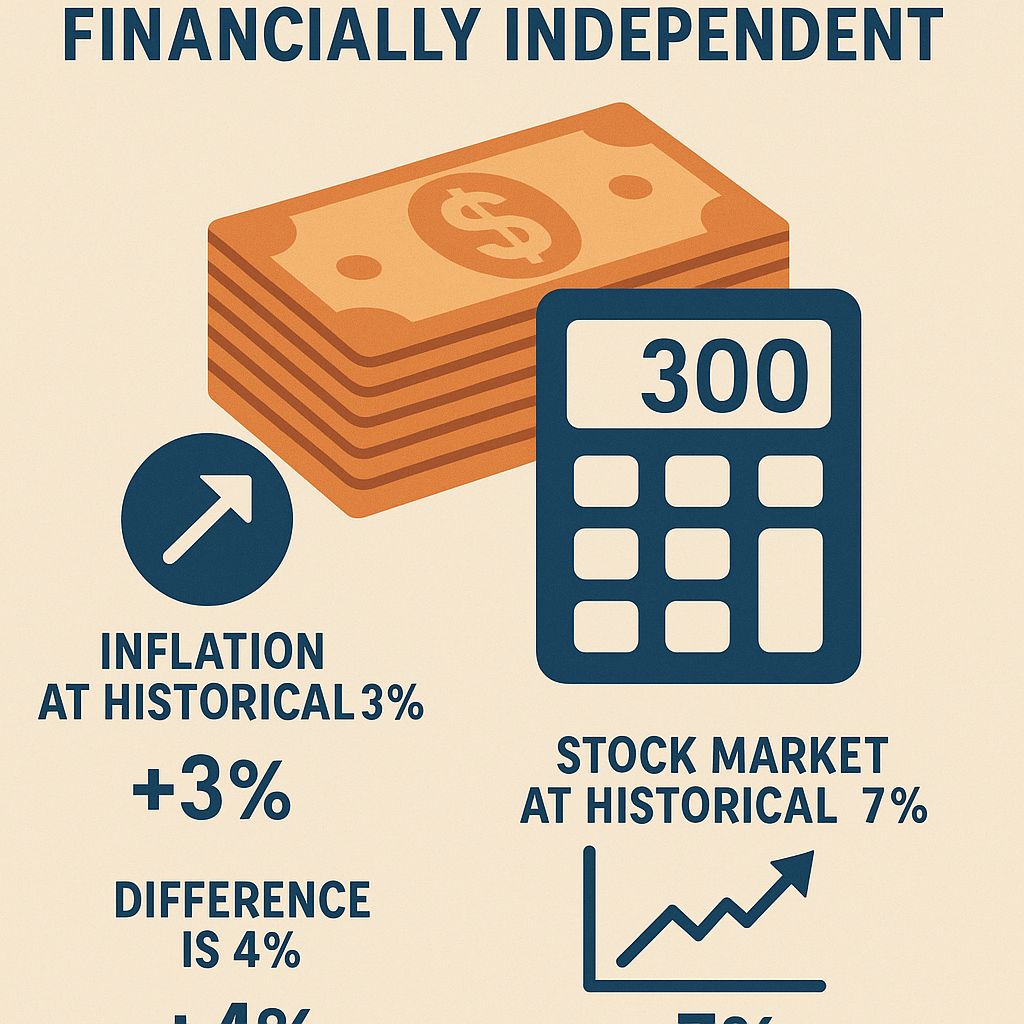

There is a rule of 300, which can help you determine how much money you will need to become financially independent. Here I explain what the rule of 300 is and how you can work it out.

Continue reading “The Rule of 300 – how much do you need to be Financially Independent?”

Here is my third property deal breakdown.

The property is a terraced house in the Bury area of Greater Manchester. The house was built around the 1880’s.

I use a financial bucket system instead of a budget. I’m not a great fan of budgets, as I find them inflexible and restrictive. Budgets that are too granular, that is, drilled down to specific spending categories, don’t consider the fluctuations in spending patterns and needs.

How do you 10x your money, for instance to turn £100 into £1000? Maybe you want to buy something that costs £1000, you only have £100 and you don’t want to use a credit card. Very sensible.

You make your money when you buy a property, so buy below market value. This is a common phrase you hear when talking about property investments and is certainly true when discussing the capital gains. It can also be true when you consider mortgage repayments, as the less you pay for the property, the less your mortgage will be.

Continue reading “How to get a Below Market Value (BMV) Property in the UK”