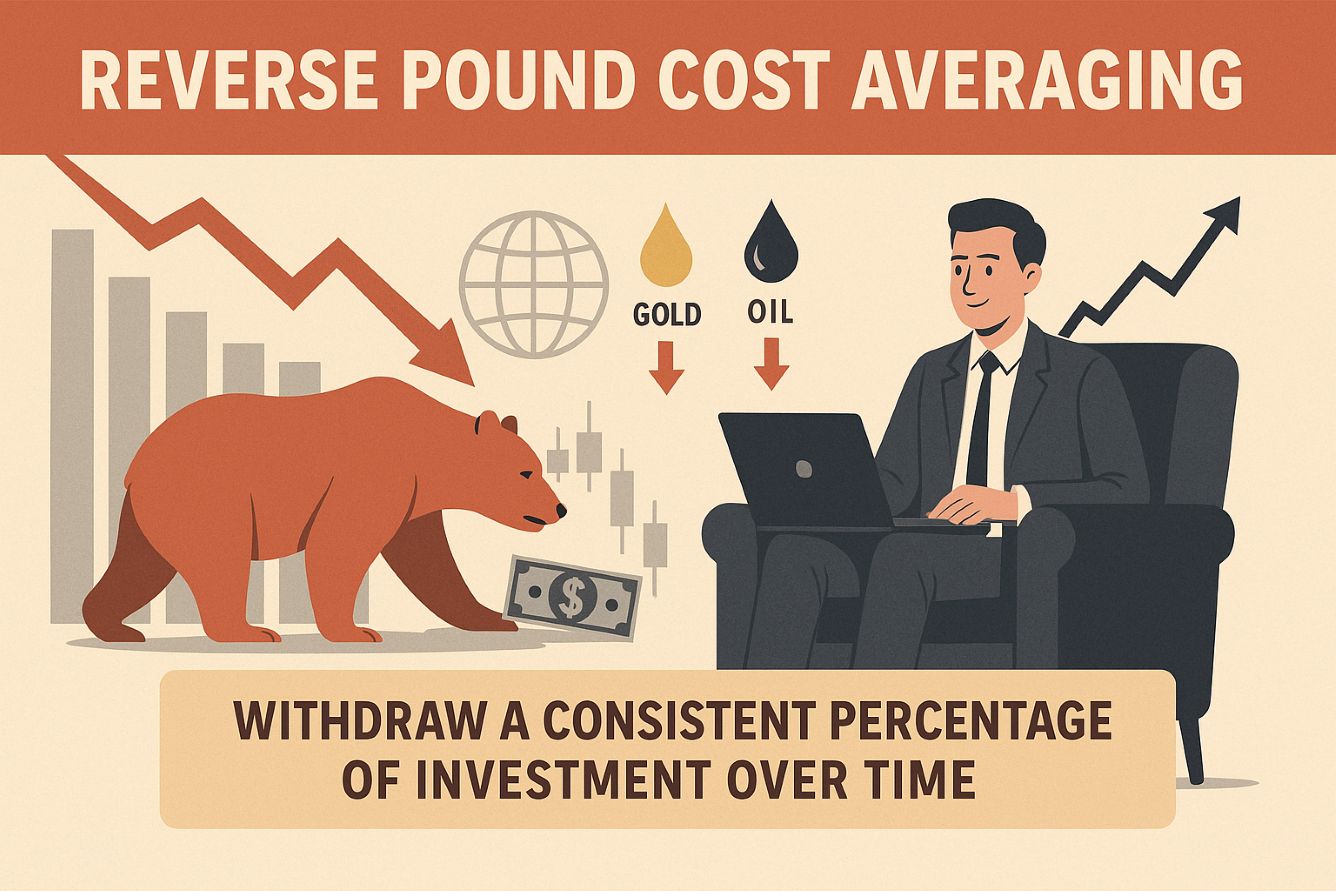

As I write this, global equity markets have slumped, wiping billions of dollars off people’s investments. Gold and oil have also fallen. There is no hiding place. However the reverse pound cost average can save the day.

Reverse pound cost average

Clear, practical steps to build wealth, protect it and get your freedom back sooner than you think.

As I write this, global equity markets have slumped, wiping billions of dollars off people’s investments. Gold and oil have also fallen. There is no hiding place. However the reverse pound cost average can save the day.

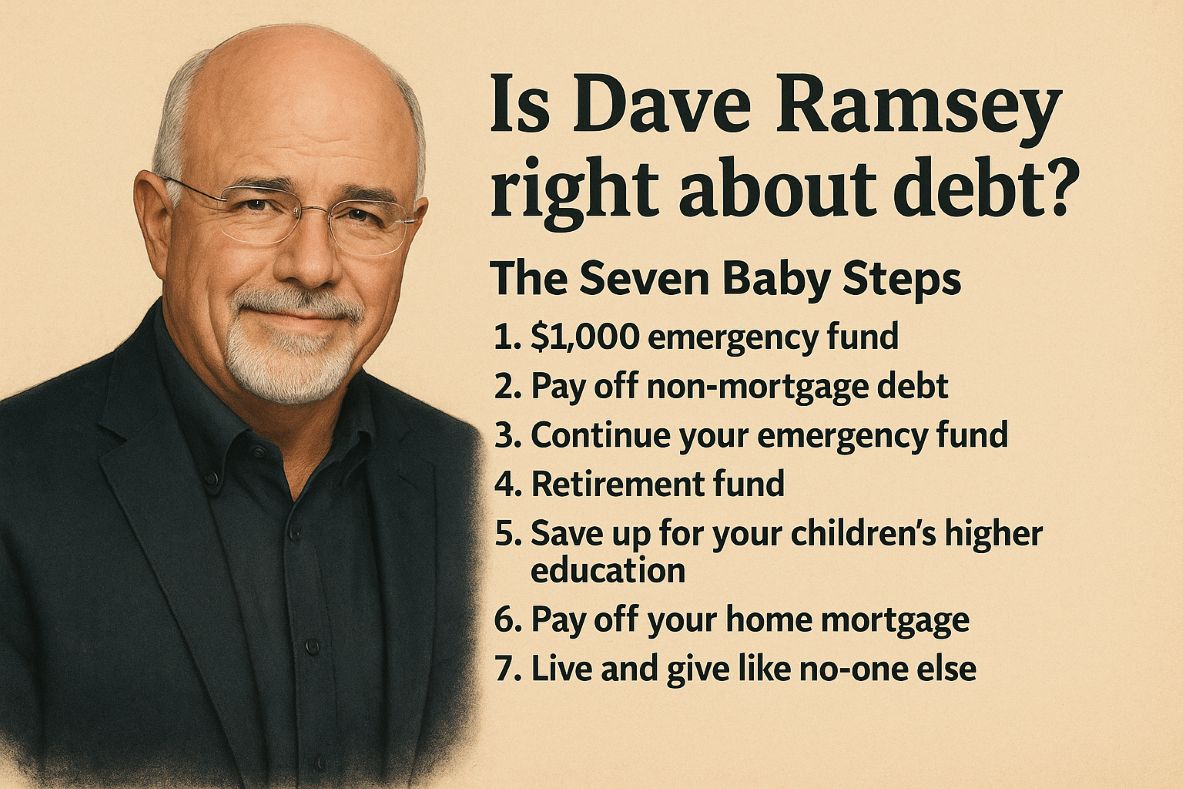

Dave Ramsey is one of the most well know teachers in the space of personal finance. I particularly like his no-nonsense approach. His financial baby step system is easy-to-follow and will allow you to become wealthy in short time.

However, is he right about what he says about debt?

I use a financial bucket system instead of a budget. I’m not a great fan of budgets, as I find them inflexible and restrictive. Budgets that are too granular, that is, drilled down to specific spending categories, don’t consider the fluctuations in spending patterns and needs.

How do you 10x your money, for instance to turn £100 into £1000? Maybe you want to buy something that costs £1000, you only have £100 and you don’t want to use a credit card. Very sensible.

Have you or are you about to come into some windfall money? Do you know what you are going to do with it? Here is a guide of what to do with windfall money.

The quickest and easiest way to accelerate the process of saving up money is to increase your income. One great way is to sell your unwanted stuff.

Here are some ways to raise extra cash quickly. Continue reading “Sell Your Unwanted Stuff or things to sell to”

The next step in getting control of your money is to use an income and expenses tracker. This is where you will record every single deposit or withdrawal from each account, including cash spending, bank accounts, savings and credit cards. Continue reading “Create an Income and Expenses Tracker”

We have now arrived at the final step of the process for achieving financial independence: Invest for Income.

All of your income, savings and investments, so far, will be funneled into a system that will invest in property. You will earn rental profits, after you have paid your expenses (see Step Eleven: Invest in Property). It will be tempting to go out and spend this income, as if it were a pay-rise, however, you’re not going to do that. You will invest for income. Continue reading “Invest for Income”

Why should you pay yourself first and what does this mean? The road to financial independence requires capital – cool hard cash. Money to give you options and to buy investments. You will only do this when you pay yourself first. Continue reading “Pay Yourself First”

On the first Saturday of each month (or whatever day you do your Weekly Review, I do a monthly financial review. It normally takes me another 30 minutes or so. This is where I record my Cash-flow Statement into an A4 notebook. I strongly recommend you start to do the same; I now have monthly Cash-flow Statements going back to 2006.

The purpose of this is extremely important; this is where you will see if you are getting wealthier or poorer. Put the previous month & year at the top of the first page, then divide the page into four equal segments. In the top left write – Income.

Top left is – Income.

Top right is – Expenses

Bottom left – Assets

Bottom Right – Liabilities.

In this segment, record all income for the month, by total for each category for example Salary and Wages, Bank Interest, Dividends, Refunds, Gifts. If you are using a software or on-line tool, this will total everything up for you and take the donkey-work out of it.

In this segment record all expenses you have incurred, again by total for each category for example Mortgage, Groceries, Child Care, Leisure, Transportation etc.

Record every asset you have as of the last day of the month for example Bank and Cash, Investments, Shares, Pension amount, Property Investment etc. You will have done this already, to establish what state your finances are in. Now you will repeat it every month. There is no need to list all of your possessions again, unless you have bought or sold a major item; Just use the figure from the original exercise.

In this segment record each liability for example Credit Card, Loans, Mortgage From this you will be able to work out the following indicators of your wealth.

In the space below the table record the following indicators:

This is simply a sum of your Assets minus any Liabilities. Your aim is to get this number into the positive and increase it.

This is Your Net worth not including your house and mortgage (as you have to live somewhere).

This is Current Assets minus current liabilities. As I said before, current Assets are things like bank and cash or any investments that you could turn into cash quickly. Current Liabilities would be things that are due soon like credit cards, but not long-term debt like mortgages and loans.

If you perform the exercises above religiously every week and month you will begin to get a real handle on your money. As your income increases you will be able to ensure that your expenses don’t spiral as well. You will also be able to budget better and spend only what you intend.

Okay I admit it may take you years to achieve financial freedom, but as my Mum says,

“Those years are going to pass anyway, so you might as well make a start.”