In this second part of the series The Smart Start Guide to Wealth in a Digital Age, I will explore what a Central Bank Digital Currency or CBDC is and why it should matter to everyday investors.

In the first post I discussed why the future of wealth is changing fast and one such change will be the CBDC.

“There is nothing either good or bad, but thinking makes it so.”

William Shakespeare – Hamlet

Like most entrepreneurs and people with a passion for wealth and financial freedom, I subscribe to many content creators across several platforms. A couple of years ago I was listening to a podcast from a financial guru, while I was driving down the motorway on a business trip. The host of the show started talking about how CBDCs were going to be forced on us and why it was such a disgrace. My heart sank when I heard about how governments will use them to control the population. Then the host said, “we need to resist these digital currencies.” He then went on to talk about hard cash and crypto.

Since that podcast, I’ve heard a lot of doom and gloom on online platforms and I became more afraid. Then it struck me. They want me to be afraid. The platforms are promoting Gold and Precious Metal brokers, Crypto-currency vehicles and other such products. They also promote fear to increase engagement.

When talking to people, who don’t listen to such material, they usually know little or nothing about CBDCs. I realised, though, that although I had heard of them and didn’t like them, I didn’t really know what they were. So, I decided to educate myself, so I could ‘know the enemy,’ so to speak. Here is what I’ve found out.

What are CBDCs

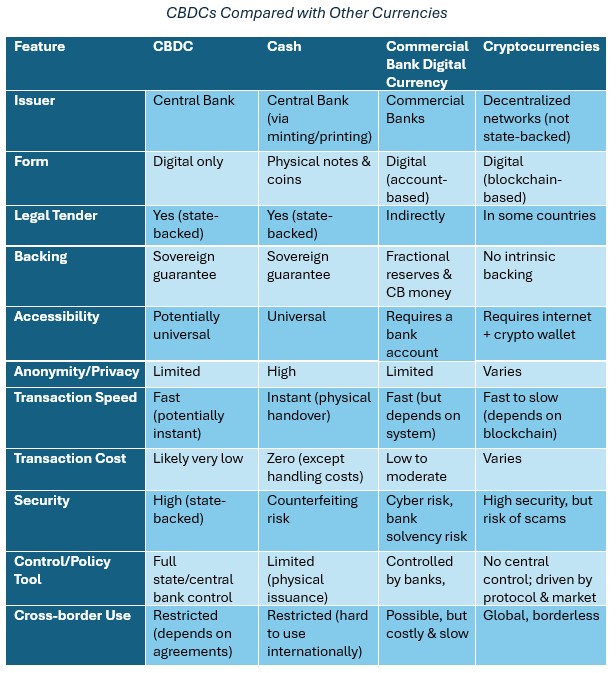

To explain what a CBDC is, it will be helpful to highlight the types of currency which will be available:

- CBDC (Central Bank Digital Currency)

- Cash (Physical Money)

- Commercial Bank Digital Currency (e.g., your online bank account)

- Cryptocurrencies (e.g., Bitcoin, Ethereum)

A Central Bank Digital Currency is a currency of money which is issued by a Central Bank, just like the notes and coins in your pocket. However, just like the money in your bank account, which is issued by commercial banks, it is digital.

The main Central Banks are The Bank of England, The Federal Reserve or the European Central Bank, although there are 222 around the world of varying size. (Source: Investopedia).

A CBDC would be different to a Cryptocurrency, such as Bitcoin, because control would be centralised and there would be no anonymity. Crypto transactions are recorded on a public ledger or Block Chain and therefore are not totally anonymous.

Like cash and your bank account money, CBDCs are also a fiat currency, which means that it isn’t backed by any physical asset such as gold or silver. This means it can be wished into existence under Government Regulation.

CBDCs would be backed by Sovereign Guarantee, which means that it will be the responsibility of the relevant government to assume liability. I.e. the buck stops with them.

As you can see from the table below, there is not a perfect currency if you are looking for safety, anonymity and control. However, the four currencies I have compared will cover all bases. I will explore in a later post in this series about how you can use all of these currencies for different purposes, along with other assets, in a resilient portfolio.

Why They Are Coming

The Bank of England stated, “We think it could help us maintain trust in money and protect our financial system, while also improving payments by increasing efficiency and helping innovation.” A look at their website also shows that their motives are to keep up with global trends away from cash and into new forms of currency. CBDC’s would increase safety and enhance payment efficiency.

CBDCs are a way of maintaining control over financial markets and many people worry that it is another way of Governments prying into our business. However, as responsible entrepreneurs that we are, we will take a honest look at how they will affect us and how we can use them as an opportunity.

What This Means For Entrepreneurs

1. Faster & Cheaper Transactions

Firstly, transactions will be cheaper and faster. Depending on the design of the system, transactions could be instant, versus normal bank transfers. Bank transfers are speedy, but there can sometimes be a delay. This could mean we have real-time payments, at all times, just like cash payments. However, you would have the advantage of remote payments.

The cost of each transaction should be very low, again this would compare favourably to bank payments where there is often a moderate fee for businesses or wire transfers.

This would also affect global trade & Forex, as cross-border payments could also become instant and cheaper. Forex businesses and international payments may need to adapt.

2. Enhanced Traceability

Every transaction would be traceable. This would have the benefit of reducing fraud but it could also increase scrutiny.

Taxes and financial reporting might become automatic; this means there will be less room for “grey area” transactions like cash.

3. Potential for Surveillance

Governments may have visibility into all financial flows. Much of the current resistance to CBDCs comes from the fact that, potentially, governments will know exactly what you are doing with your money. This may impact businesses who want to guarantee anonymity to their clients. There are also fears that this could open the door to a Social Credit system, where governments can nudge people’s behaviours by punishing certain types of purchase. Some people also fear that we could see automatic fines, for example, overstay on a carpark and a fine could be taken from your account automatically.

4. New Business Models

CBDC’s would certainly encourage new business models. Potentially you could have micropayments such as pennies or fractions of a penny. Micro payments are not always viable, currently, because the cost of transaction is prohibitive. Off the top of my head, let’s say you could pay a penny to remove an advert from a website.

Programmable money

CBDC’s could be programmed to perform certain functions or self-execute rules. For instance, you could have money that expires after 30 days. Could you also see a scenario, where a parent gives ‘pocket money’ that couldn’t’ be spent on certain things? Or, could a government issue money that can only be spent on essentials?

You could also theoretically programme money to only be used by the receiver once a certain condition has been met, such as receipt of goods or service. This could reduce fraud.

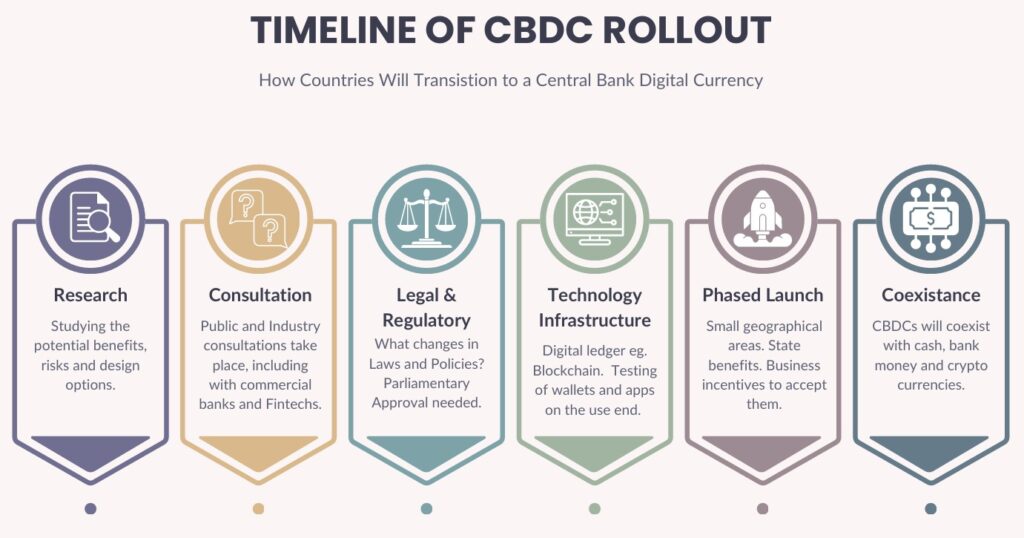

How A Country Transitions To A CBDC

1. Research & Consultation Phase

We are currently in the research and consultation phase. The central banks are studying the potential benefits, risks, and design options. The Bank of England states that it ‘hasn’t made a decision yet’ on whether to introduce a CBDC, but they are testing the feasibility of them. In the UK, parliamentary approval would need to be given. You could see this issue becoming a political football.

Public and industry consultations take place, including with commercial banks, fintechs and businesses. Once approved, the next step will be to run pilot programs that will be run in a limited region or sectors.

2. Legal & Regulatory Adjustments

The Bank of England is currently in the design stage. This involves reviewing what technology and policies may be needed to use a CBDC. There would also be a change in the law to define the CBDC as legal tender.

Not only would the laws around legal tender need to be reviewed, but there would need to be robust frameworks, put in place, to protect privacy and security. They would also need to make sure anti-money-laundering (AML) is included in this.

Before anything is launched, Parliament would need to approve it. There would also be a raft of public consultation as various public and private bodies will surely want a say.

3. Technology Infrastructure

There would need to be a national digital ledger created. This may or may not be blockchain. Companies are working on this now, but before any launch they would have to ensure that everything is safe and tested.

From the user end, apps and wallets will need to be developed to hold and transfer the digital money. Again, these will need to be assessed in the real world before launching.

Commercial banks may serve as intermediaries in a two-tier model, or the central bank itself may distribute digital currency directly, in a retail model. If commercial banks are involved, each one of those will also need to ensure they have the same level of robustness with their systems.

The upshot of all this is that the roll-out will not be quick and will be phased.

4. Phased Rollout of CBDC

After testing in a small geographical area or sector, the first phase of the roll out will be Government payments. Recipients of benefits or state pensions might be the first to have the CBDC. This would obviously need businesses to accept them and they would be encouraged to do so, with incentives.

Once a period of time has gone on with this phase, the CBDC will be rolled out to the rest of the population. Eventually, the CBDC will coexist with cash and digital bank money.

Bottom Line

CBDCs are coming, not tomorrow, but within 5–10 years for many developed countries. It will be much sooner for some countries. As an entrepreneur, early positioning is key. Rather than resist the change, lean into understanding it, adapting quickly, and helping others do the same. That’s where the real leverage lives. I will be continuing this theme in the upcoming posts, showing you how you can adapt and thrive in this new age.

As Hamlet might advise us: there is an equal upside and downside, it all depends on your outlook.